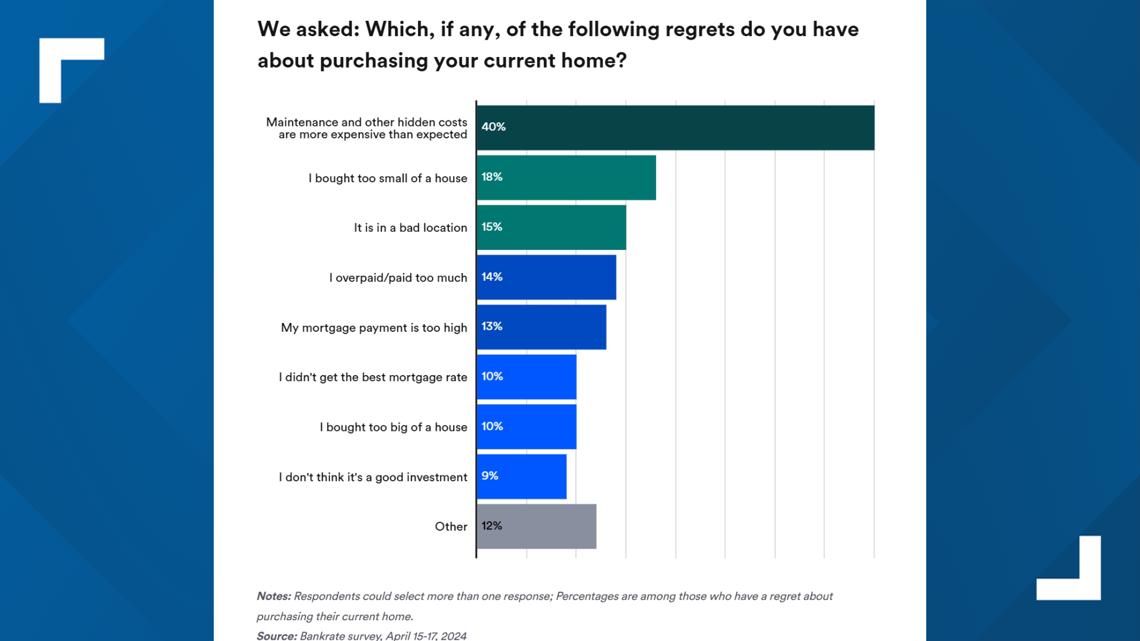

Among homeowners with regret, 42% say maintenance and other hidden costs are more expensive than expected.

WASHINGTON — Owning a home is the cornerstone of the “American Dream.” Homeownership symbolizes stability, financial success, and a personal stake in your community.

But according to a new Bankrate survey, almost half of the homeowners it surveyed say they have at least one regret about the purchase of their home.

“Our survey finds that the number one regret among homeowners who have a regret is the cost of maintenance and other so-called hidden costs,” said Mark Hamrick, a Senior Economic Analyst with Bankrate. “So that’s really about affording the ownership of a home once you’ve made the purchase. I think one of the things that many homeowners don’t necessarily take into consideration is what goes along with the mortgage payment, and that is property taxes and the cost of insurance.”

Among homeowners with some type of regret about the purchase of their current home, buying too small of a house (21%) was the second most common regret after costlier-than-expected maintenance and hidden costs.

Other regrets include the mortgage payment being too high (16%), overpaying or paying too much for the house (15%), buying a house in a bad location (14%), buying too big of a house (11%), not getting the best mortgage rate (10%), and not thinking it’s a good investment (6%).

The survey also revealed that regrets for certain aspects of homeownership vary by generation. Older homeowners are more likely to regret high maintenance costs, and younger generations are more likely to regret high mortgage payments

More than half of current homeowners (55%) say they do not have any regrets about purchasing their current home. This tendency rises with age, with baby boomer homeowners (58%) the most likely to express no regrets, followed by slightly more than half of millennial homeowners (54%) and 52% of both Gen X and Gen Z homeowners.

Here are a few tips to help homeowners have the least amount of regret:

- Plan Ahead: Set some money aside ahead of time so you’re prepared for unexpected expenses or home repairs.

- Consider Your Options: Carefully consider what you need in a home and what you don’t. Scaling down will help you save money down the road.

- Negotiate: The sale price might not be as fixed as you think

- Shop lenders: Don’t go with the first mortgage rate quote you receive

“Home ownership is equated with the American dream, but we don’t want this to be sort of a bit of a nightmare where people don’t fully consider the range of costs,” Hamrick said.

If you are in the market for a new home and trying to figure out how much house you can afford, Bankrate says you want to use the 28/36 rule of thumb.

- Don’t spend more than 28% of your gross monthly income on housing costs

- Don’t spend more than 36% on all of your debt combined, including those housing costs: principal, interest, taxes, and home insurance.

Here is Bankrate’s mortgage calculator.

link